24 May 2026

News

Google’s AI blizzard

Google held its annual ‘IO’ developer event/product launch, and as ever there were hundreds of different announcements. It’s probably worth watching the entire two-hour keynote, but there are two things worth calling out. First, incumbents always try to make the new thing a feature, but sometimes they’re right: Google has a huge number of products and surfaces, and it’s adding AI features to all of them.

But second, Google is pushing all the way to change search from navigation to synthesis and summary. Search results haven’t been the plain vanilla ’10 blue links’ for a long time, as Google created vertical structured products around eg restaurants, but now the search box itself will become dynamic, morphing and changing into new forms and generating its own little widgets and tools. On the other side, you’ll be able to set up your own ‘agents’ that keep track of new results and tell you when things change (though this demo seemed extremely geeky).

For all of this, Google continues to shift emphasis from taking you to a resource made by someone else to generating its own summary or version of the answer, made from everything it’s seen on the web. Google will tell you the answer, based on the averages of everything other people have made. If you search for a ‘how to’, YouTube will take you to the right place in the video (YouTube itself has replaced a lot of web pages for content that doesn’t necessarily need to be video, because content creators can access a network, a recommendation system, and of course, a direct revenue payout). Next year, it might make you a video.

As many people have discussed in the last year or two, this is a pretty direct challenge to the implicit social contract of search: that publishers let Google index their content (and make money from ads on that) and in exchange, Google sends them traffic. Now every publisher is thinking about ‘Google Zero’ - no traffic from search at all. But then, how does the web work? Ironically, this is a function of competition: if Google doesn’t do this, OpenAI will, if this is where the users are going. But I don’t think anyone really knows what this means. KEYNOTE, SEARCH

SpaceX

SpaceX filed for an IPO. You can read the document here, and see this week’s column. LINK

For reference, a useful paper on the case for AI data centres in space. LINK

Quarterly numbers

Over the last two years, OpenAI and Anthropic have from time to time given numbers for ‘annualised revenue’, which generally takes the previous four weeks and multiplies by 13, though OpenAI gives a number net of payments to its partners and Anthropic has been giving a gross number. Now, as they both (especially OpenAI) get close to filing for an IPO, quarterly numbers are leaking. The WSJ says Anthropic has $4.8bn revenue in Q1 and will hit $10.9bn in Q2, with a small operating loss in Q1 and $559bn operating profit in Q2. (Meanwhile, it’s been widely reported that the annualised revenue number has now hit $45bn.) The Information reports OpenAI had $5.7bn revenue in Q1, with a negative 122% ‘adjusted operating margin’. None of this is GAAP, obviously. These companies are still burning enormous amounts of cash to deliver that revenue, but if you’re thinking that this isn’t really useful, this level of customer spending should wake you up. ANTHROPIC, OPENAI

Tokenmania

The tech industry is in a severe supply/demand crunch, as agentic coding works so well that usage is suddenly massively ahead of available capacity (I touched on this in my new presentation - I think this is temporary and will play out like mobile data). This week, Marc Benioff at Salesforce says he expects to spend $300m on Anthropic tokens this year (though really, who knows?), OpenAI announced an option to buy guaranteed capacity (which is probably a good buy in the short term and a bad buy in the long term), and OpenAI also said it would give $2m of free tokens to every company in the current YC batch (customer acquisition). SALESFORCE, CAPACITY, YCOMBINATOR

Unwinding Manus

Last month, the Chinese government ordered the cancellation of Meta’s acquisition of Manus, but given it has already been completed and the tech and team absorbed, it was hard to know how to comply. Now Bloomberg reports that the three founders are in talks to raise at least $1bn from Chinese investors to buy it LINK

The week in AI

Donald Trump’s AI regulation executive order was suddenly postponed, apparently after a bunch of tech execs grabbed the phone. (Just a thought, but perhaps the US court could try having one of those ‘legislature’ things, where you could elect a bunch of thoughtful and moderate people to spend time working out what laws should be and then passing them, in some kind of coherent, transparent process?) LINK

Bloomberg says that Cursor, the coding company now in a deal with xAI, reached $3bn annualised revenue in late April. LINK

Andrej Karpathy, a leading AI researcher and a prominent independent voice, decided to take a job at Anthropic. LINK

Google and Blackstone are doing a $5bn JV to create an AI neocloud built on Google’s TPU chips. Google wants more volume on TPU production and more developers using them, plus this is a way for Google to serve more AI demand without taking the infrastructure onto its own balance sheet. LINK

Ideas

Things that are obvious when you think about it - a lot of those bland would-be thought leader pieces on LinkedIn are written to order in content mills in the Philippines. LINK

Continuing the industry’s digestion of the Anthropic Mythos cyber story, Cloudflare released a pretty useful analysis. LINK

Apple’s latest accessibility release showcases a lot of generative AI that doesn’t look like AI - it’s just an enabling technology used to create a new feature. LINK

The US CAIS group (part of NIST) evaluates the latest Deepseek model as about eight months behind the (US) frontier. LINK

Outside interests

A very cool Richard Sapper ‘sound book’ I’ve never seen before. LINK

A reminder of the brilliant 1988 LA Times /Sid Mead concept of what 2013 would look like. Amongst other things, newspapers faxed to your home. LINK

Data

London and New York public transport use seems to have settled at 70-80% of the pre-pandemic peak, reflecting (mostly) WFH. Fridays are down 40%. LONDON, NYC

AI has resulted in a surge of people representing themselves in court. This is probably all about the balance - how much is this increased access, versus frivolous cases with no cost threshold or legal errors wasting court time or worse? LINK

A third of Walmart operating income now comes from the third party e-commerce marketplace, advertising and membership. LINK

Omeda’s media audience report. LINK

Global entry-level (<$100) smartphone markets are shrinking as the AI capex surge means the OEMs can’t get memory at the right price. LINK

Column

SpaceX

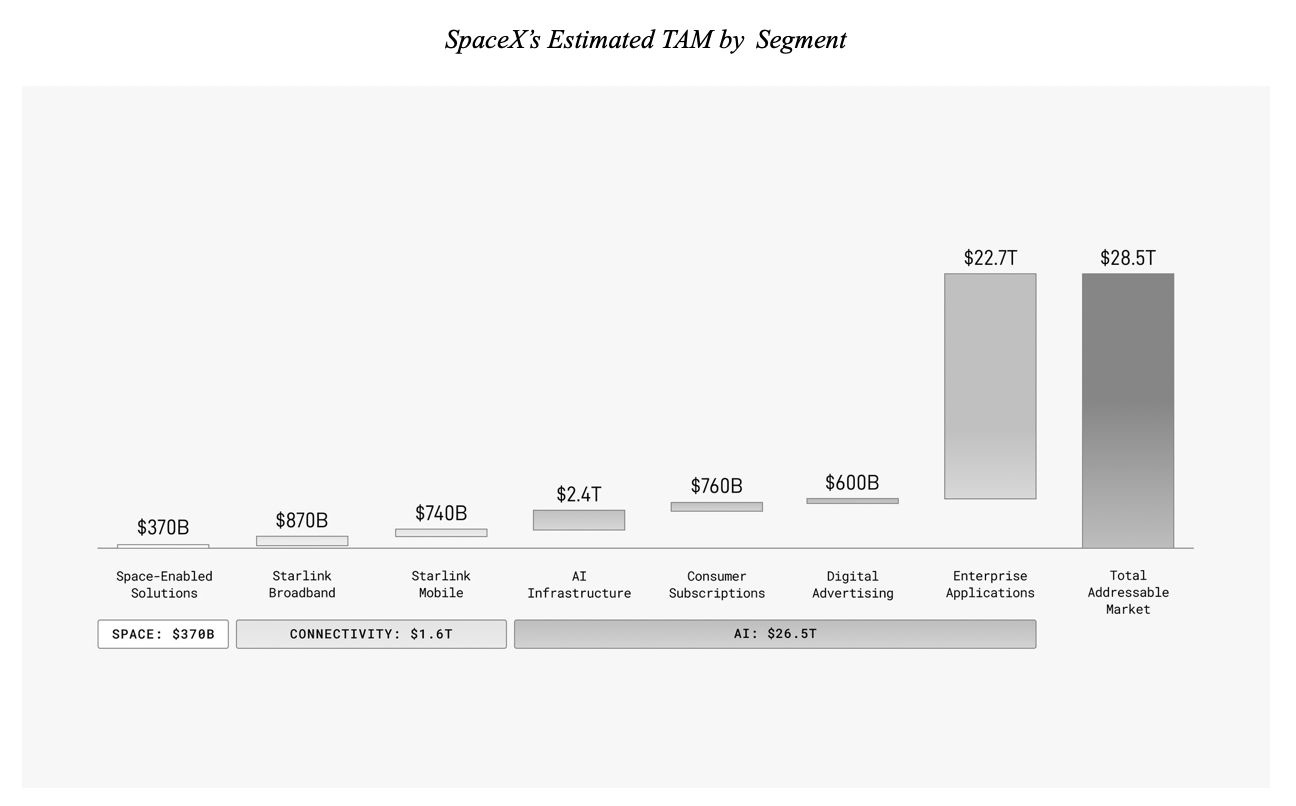

First, let’s start with the TAM chart for SpaceX’s S1 filing, because that’s what everyone is looking at, so you need to have seen it too.

Now let’s talk about what this means.

Tesla and SpaceX are pretty much the same company. Each of them started from the idea that something people had talked about for decades might actually work now, and then Elon Musk turned that idea into an actual working product and a real company operating that idea at scale. This is really, really hard.

However, in both cases, it also turned out that while this was amazing, it wasn’t actually an amazing business, but meanwhile, there’s a lot else being promised.

So, Tesla had revenue of $100bn in the last 12 months - a scaled car company! But that produced net income of $4bn and revenue has been flat for three years, with all the growth in EVs going to the new wave of Chinese OEMs, who will take a big chunk of the market everywhere that Tesla isn’t protected by tariffs. EVs are really hard for the incumbent OEMs’ disaggregated model, but they aren’t hard (or hard enough) for the Chinese manufacturing complex, and Tesla doesn’t have a competitive advantage against Chinese EVs.

But if you look at any financial analyst’s Tesla valuation (or rather, their attempts to ascribe financial reality to the current market cap, of $1.6tr), then you’ll see they ascribe no more than 10-15% of the valuation to the car business - all the rest is for businesses that don’t really exist yet: mostly, a Tesla autonomy ‘robotaxi’ (where Elon Musk has been promising autonomy ‘next year’ for a decade without ever quite delivering) and humanoid robots (will this even be a real market? How does Tesla beat the dozens of Chinese companies already selling this?).

Now see SpaceX. Self-landing reusable rockets! We should all pause for a moment of awe. SpaceX has cut the cost of getting mass to orbit by at least 90% and is pushing it further. LEO satellites are cheap now. But what kind of business is that? What’s the price elasticity of LEO orbit? Well, the launch part of SpaceX had revenue of $4bn last year, up 7.6%, it seems mostly from US government contracts: who else wants satellites? But connectivity (both StarLink and dead-spot cellular partnerships) was $11.4bn, up 50% year-on-year. This is a good business. But how big? It’s never going to replace FTTH for consumer broadband, for example. There’s plenty of speculation about what else you could do in orbit (growing exotic molecules, or metals for manufacturing, say), but no-one knows if those are big or even real. So this is all very cool, but just as the cars are a small part of the Tesla story, this is a small part of the SpaceX story, because it needs something bigger, and as we see above, the bigger story is AI.

First, Elon Musk obviously wants to turn xAI, now part of SpaceX, into a competitor to OpenAI and Anthropic, both now valued in private markets at close to $1tr. Unfortunately, the entire founding team quit and the giant datacentre they built with such pride had to be rented out to Anthropic (at $15bn a year, we learn from this filing, which is more than the rockets and Starlink combined). Musk has bounced back from worse than that, but clearly it’s not there now.

And second, we can solve the problem of power and cooling for data centres (though cooling isn’t a real problem and it's not clear how much power is either) by building them in space and using free solar and IR cooling. And that, plus little things like mining minerals on Mars, produces that $28.5tr TAM. And so just as Tesla is an ex-growth car company at 4% margin with a bunch of big promises, so SpaceX is a nice little launch business with a niche connectivity service, and a bunch of really big promises.

The pattern, as we all know, is that Elon Musk raises funding to build X by promising Y, and X often arrives years late (if ever - remember the Roadster? The mass-market car? Solar roofs? Hyperloop? Tunnels? Autonomy?), and maybe only half of what was promised… but half of X is still amazing, Y is coming soon (honest!) and meanwhile he’s promising Z, which is even more amazing. And as long as people are willing to invest in the promise of Z, it doesn’t matter that X, amazing as it was, ended up flat.

But perhaps that isn’t really the point. The striking thing about SpaceX is how much it all presumes the end-goal. The explicit aim of SpaceX is not to maximise shareholder value: it’s to go to Mars and turn humanity into a ‘multi-planetary civilisation’. So, we need rockets. How do we pay for that? A satellite internet service! Now we need bigger rockets! How do we pay for that? Build an AI company! The whole thing is a self-fulfilling prophecy, except that the end-goal is to have a few people living in tin cans on a frozen rock 200 million miles away. That sounds more like Weyland-Yutani.